11.25.2025

Market Insights – 11/25/25

Wholesale Prices, Week Ending November 22nd, 2025

The Canadian used wholesale market saw a decline of -0.44% in pricing for the week. Car segments prices decreased by –0.33% while the Truck/SUV segments decreased by -0.53%. The largest declines in the Car segments were seen in Full-Size Car at -0.65% and Compact Car with -0.44%. The largest declines in the Truck/SUV segments were Small Pickup with -1.26% followed by Full-Size Pickup at -0.98%.

| This Week | Last Week | 2017-2019 Average (Same Week) | |

| Car segments | -0.33% | -0.34% | -0.38% |

| Truck & SUV segments | -0.53% | -0.53% | -0.17% |

| Market | -0.44% | -0.44% | -0.27% |

Car Segments

- Last week there was an overall depreciation of -0.33% noted in car values. All segments showed this movement.

- Segments with the largest declines were Full-Size Car (-0.65%) followed by Compact Car (-0.44%) and Prestige Luxury Car (-0.38%).

- The smallest declines were Sub-Compact Car (-0.20%) and Mid-Size Car (-0.22%).

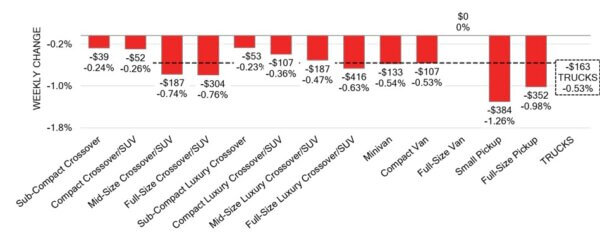

Truck / SUV Segments

- Truck segments had an overall decline of -0.53% in values. Twelve of the thirteen segments reflected this.

- Those with the largest depreciations were noted in Small Pickup (-1.26%), Full-Size Pickup (-0.98%), Full-Size Crossover/SUV (-0.76%) and Mid-Size Crossover/SUV (-0.74%).

- Categories with the least notable drops were Sub-Compact Luxury Crossover (-0.23%) and Sub-Compact Crossover (-0.24%).

Wholesale

The Canadian market continues its downward trend, with results similar to those seen last week. Car segment values shifted by 0.01% this week, bringing the total decline to –0.33%. Truck segment performance varied across the board but collectively resulted in a –0.53% decline. Just over 59% of market segments recorded an average value change exceeding ±$100. Monitored auction sale rates this week varied between 14.6% and 59.1%, averaging at 42.1%. Sales rates across auction lanes have shown ongoing fluctuations, influenced by economic uncertainty, political factors, and sellers maintaining firm floor prices. Supply has stabilized and returned to regular levels; however, upstream channels continue to hold priority sale access to inventory. Buyer demand for high-quality vehicles at auctions on both sides of the border persists.

Used Retail Prices & Listing Volume

The average listing price for used vehicles is slightly decreasing, as the 14-day moving average was at $36,980. This analysis is based on approximately 216,760 used vehicles listed for sale on Canadian dealer lots.

Market Insights

Economics & Government

- Canada’s headline inflation rate eased to 2.2% in October 2025, down from 2.4%

in September, moving closer to the Bank of Canada’s 2% target as anticipated in

its baseline economic scenario. - Foreign investors increased their holdings of Canadian securities by $31.32

billion in September 2025, up from an upwardly revised $23.6 billion in August,

marking the highest level of investment since April 2024. - Housing starts in Canada dropped 17% year-over-year to a seasonally adjusted

annual rate of 232,765 units in October 2025, marking the lowest level in seven

months. - Retail sales in Canada were set to have remain unchanged from the previous

month in October of 2025, according to a preliminary estimate. - The yield on the Canadian 10-year government bond increased to 3.21%.

- The Canadian dollar is around $0.709 this Monday morning, down slightly from

$0.714 a week prior.

U.S. Market

- The market declined again last week as Car values fell -0.66% and Truck/SUV values dropped -0.93%. Full-Size Cars and Sub-Compact Luxury Crossovers posted the largest segment declines. The auction conversion rate remained steady at 56%, reflecting continued buyer selectivity and firm floors. Clean, retail-ready units drew the strongest engagement, while average-mile vehicles required additional pricing flexibility. Newer 2024–2025 models continued to show softness.

Industry News

- Canadian ZEV market share reached its highest point of 2025 in September. Still down against a financially supported 2024 comparison, ZEV sales accounted for 10.2%, its highest level since January when the iZEV rebate was discontinued mid-month.

- British Columbia announced it will not be reinstating its provincial ZEV rebate, that provided up to$4,000 to qualifying vehicles/consumers. The rebate program which was paused back in May follows news that the provincial ZEV mandate in B.C. will be scaled back as well, with a decision to be made on a new mandate next year that should align with the federal decision that has yet to be made.

- Jeep released its latest EV and first to be trail-rated to its lineup, with the Jeep Recon. This model is geared for off-roading, producing a range of up to400km with 650hp and 620 lb. ft. at your disposal. With a U.S. starting price of $66,995, this will not provide an affordable EV option for the Jeep brand as we await Canadian pricing later.

- Infiniti is planning a performance product offensive with the German brands in its crosshairs. The brand announced at SEMA that it will begin executing on a strategy to develop low-volume, high-revving variants of current and future models, aimed at the likes of BMW’s M and Mercedes-Benz’s AMG product lines.

- Another mainstream spun-off luxury is planning a performance focused offering to fight against European brands. Genesis released the GV60 Magma EV, which officially launches the performance ‘Magma ‘line in the flesh with a650hp version of the EV. This comes as an introduction to the Magma GT concept illustrates the seriousness of this effort to the industry, with plans to produce it as a ‘halo’ vehicle in the coming years.