12.23.2025

Market Insights – 12/23/25

Wholesale Prices, Week Ending December 20th, 2025

The Canadian used wholesale market saw a decline of -0.48% in pricing for the week. Car segments prices decreased by –0.38% while the Truck/SUV segments decreased by -0.61%. The largest declines in the Car segments were seen in Full-Size Car at -1.49% and Compact Car with -0.79%. The largest declines in the Truck/SUV segments were Compact Van with -1.77% followed by Minivan at -1.37%.

| This Week | Last Week | 2017-2019 Average (Same Week) | |

| Car segments | -0.38% | -0.46% | -0.45% |

| Truck & SUV segments | -0.61% | -0.52% | -0.31% |

| Market | -0.50% | -0.50% | -0.38% |

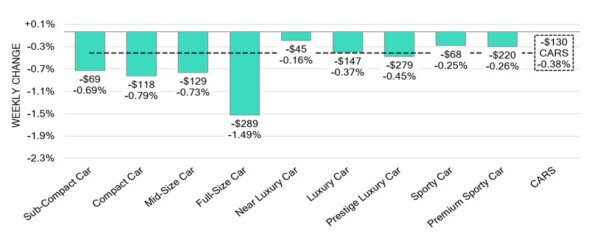

Car Segments

- Last week values softened, with the overall car market down 0.38% as depreciation remained widespread.

- The largest declines were led by Full-Size Car (-1.49%), Compact Car (-0.79%), and Mid-Size Car (-0.73%), with Sub-Compact Car (-0.69%) also posting a notable drop.

- The smallest movements were seen in Near Luxury Car (-0.16%), Sporty Car (-0.25%), and Premium Sporty Car (-0.26%).

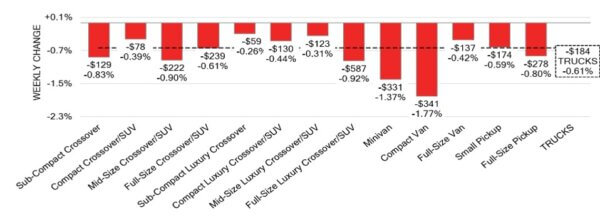

Truck / SUV Segments

- Last week values softened, with the overall truck market down 0.61% as declines deepened slightly across most segments.

- The steepest drops were led by Compact Van (-1.77%), Minivan (-1.37%), and Full-Size Luxury Crossover/SUV (-0.92%), with Mid-Size Crossover/SUV (-0.90%) also showing a sizable decline.

- Segments with the smallest declines were seen in Sub-Compact Luxury Crossover (-0.26%), Mid-Size Luxury Crossover/SUV (-0.31%), and Compact Crossover/SUV (-0.39%).

Wholesale

The Canadian market’s downward trend carries on, with comparable results to the week prior. Truck segment values recorded a 0.09% adjustment, bringing the total decline to –0.61%. Similarly, car segment values shifted by 0.08%, bringing the total decline to –0.38%. Just over 77% of market segments recorded an average value change exceeding ±$100. Monitored auction sale rates this week varied between 18.8% and 82.5%, averaging at 49.5%. Sales rates across auction lanes have shown ongoing fluctuations, influenced by economic uncertainty, political factors, and sellers supporting firm floor prices. Supply has stabilized and returned to regular levels; however, upstream channels continue to hold priority sale access to inventory. Buyer demand for high-quality vehicles at auctions on both sides of the border persists.

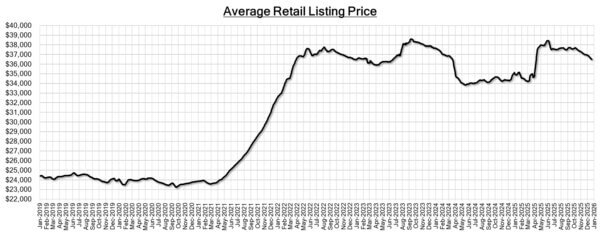

Used Retail Prices & Listing Volume

The average listing price for used vehicles is slightly decreasing, as the 14-day moving average was at $36,550. This analysis is based on approximately 199,000 used vehicles listed for sale on Canadian dealer lots.

Market Insights

Economics & Government

- The Bank of Canada held its target overnight rate at 2.25% in December 2025,

maintaining the Bank Rate at 2.50% and the deposit rate at 2.20%, after

indicating in October that the policy rate was appropriately positioned. - Canada’s trade balance shifted to a $0.15 billion surplus in September 2025,

reversing a $6.3 billion deficit in August and sharply beating expectations for a

$4.5 billion shortfall. It marked the nation’s second trade surplus of the year. - Canada’s exports jumped 6.3% month-over-month to C$64.2 billion in September

2025, rebounding from a 3.2% decline and posting the strongest monthly gain

since February 2024. - Housing starts in Canada rose by 9.4% month-over-month in November 2025,

rebounding from a 17% drop in October to reach a seasonally adjusted annual

rate of 254,058 units, slightly exceeding the market forecast of 250,000. - The yield on the Canadian 10-year government bond increased to 3.37%.

- The Canadian dollar is around $0.726 this Monday morning, up slightly from

$0.722 a week prior.

U.S. Market

- Wholesale values eased modestly last week, with Cars down –0.50% and Trucks/SUVs down –0.48%, reflecting continued but orderly year-end softening. The auction conversion rate declined to 57%, down from 59% the prior week, as overall selective bidding returned amid mixed-condition inventory. Despite the slower sell-through, clean late-model units continued to attract strong competition, keeping market tone stable though increasingly condition-sensitive.

Industry News

- Ford Motor Company announced it will be discontinuing the F-150 Lightning EV Pick-up, as it looks to change its strategy to bring more gas/hybrid vehicles to market. This change will result in charge-offs amounting to$19.5 billion, as the next version of the Lightning will now become an extended range EV (EREV), similar to Ram’s new direction.

- Nissan Motor Company is looking to vastly expand its lineup of Nismo-enhanced performance vehicles. Up until recently, they were produced for rare enthusiast vehicles and one-off trims. As this product offering grows from 5 to 10 models in a global push for high-performance variants of current and future models.

- The European Union is looking to roll back its ICE ban originally set for 2035. It’s now discussing the sale of up to 35% gas cars after the Jan. 1, 2035, deadline. This is the result of reducing CO2 targets 10%, allowing flexibility in the market to sell gas models after 2035.

- Canada’s Q3 results show an expected decline year-over-year for EV registrations as they fell by 50%. Hybrids accounted for 12.4% vs. 9.6% last year, and plug-in hybrids were almost exactly the same as in 2024, at 3.8%. EVs saw only 5.5% compared to 11.6% 12 months ago, as gas vehicles edged up in market share to 73.8% on a very stable annual quarterly registrations comparison.

- Despite the implications and increased cost of tariffs, Ford will continue its plan to retool the Oakville, ON assembly plant to produce its Heavy-Duty Pick-up Trucks.

- Stellantis also provides some hope in Canadian vehicle manufacturing as its Windsor, ON plant adds a third shift. This comes as the brand fails to commit production plans at its Brampton, ON facility which shared that upcoming Jeep Compass assembly will move to Illinois.

Editor’s Note: This is our final Black Book Weekly Market Update of 2025. We will pause publication during the holiday period and resume regular weekly reporting on January 6, 2026. Thank you for following our insights throughout the year.