03.10.2026

Market Insights – 3/10/26

Wholesale Prices, Week Ending March 7th,2026

The Canadian used wholesale market saw a decline of -0.30% in pricing for the week. Car segments prices decreased by –0.61% while the Truck/SUV segments decreased by -0.03%. Mid-Size Crossover/SUV segment saw the biggest increase of +0.47%. The largest declines in the Car segments were seen in Prestige Luxury Car at -0.94% and Luxury Car with -0.85%. The largest declines in the Truck/SUV segments were Compact Van with -1.70% followed by Sub-Compact Luxury Crossover/SUV at -0.97%.

| This Week | Last Week | 2017-2019 Average (Same Week) | |

| Car segments | -0.61% | -0.58% | -0.16% |

| Truck & SUV segments | -0.03% | -0.34% | -0.21% |

| Market | -0.30% | -0.45% | -0.18% |

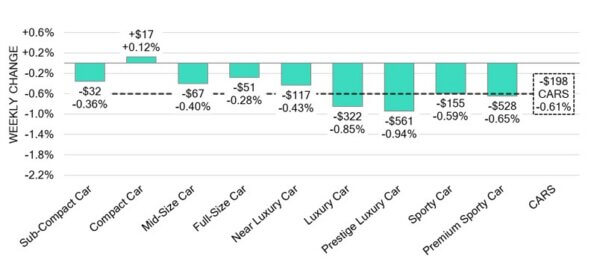

Car Segments

- Last week values declined in the car segment, with overall prices declining 0.61%.

- The largest depreciations were in Prestige Luxury Car (-0.94%), Luxury Car (-0.85%), and Premium Sporty Car (-0.65%), followed by Sporty Car (-0.59%).

- The smallest declines were seen in Full-Size Car (-0.28%), Sub-Compact Car (-0.36%), and Mid-Size Car (-0.40%), while Compact Car posted a gain (+0.12%).

Truck / SUV Segments

- Last week truck values softened overall, declining 0.03% across the segment.

- The largest drops were seen in Compact Van (-1.7%), Sub-Compact Luxury Crossover/SUV (-0.97%), and Compact Luxury Crossover/SUV (-0.83%).

- Seven segments contradicted the trend. Of those are Mid-Size Crossover/SUV (+0.47%), Minivan (+0.44%), Full-Size Pickup (+0.36%) and Full-Size Luxury Crossover/SUV (+0.16%).

Wholesale

The Canadian market’s decline continues, though at a slower pace and showing a noticeable shift from the previous week. Truck segment values reflected a 0.31% shift bringing the total change to –0.03%. Car segment values presented a 0.03% change, resulting in a total decline of –0.61%. Exactly 50% of market segments saw average value movements greater than ±$100. Auction sale rates across monitored lanes ranged from 29.6% to 76.1%, resulting in a 48.8% average. Sales rates across auction lanes continue to fluctuate, driven by political factors, economic uncertainty, and sellers supporting firm floor prices. Auction inventory has returned to normal levels, experiencing a small uptick, however upstream channels continue to hold priority sale access to inventory. Buyer demand for high-quality vehicles at auctions on both sides of the border persists.

Used Retail Prices & Listing Volume

The average listing price for used vehicles is slightly decreasing, as the 14-day moving average was at $37,100. This analysis is based on approximately 199,000 used vehicles listed for sale on Canadian dealer lots.

Market Insights

Economics & Government

- Markets have reacted strongly to the war in the Middle East between the US and

Iran. Higher oil prices have triggered an increase in gas prices which are up at

least 10 cents per litre over the past week. Diesel prices have spiked even higher

and could pass the $2 per litre mark next week. - Higher prices for gas and diesel risk triggering a new round of inflation and could

force the Bank of Canada to start raising interest rates - The yield on Canadian 10-year government bonds have increased to 3.17%.

- The Canadian dollar is around $0.733 this Monday morning, an increase from

$0.731 a week prior.

U.S. Market

- Auction activity remained strong last week, with solid buyer participation and healthy sell-through rates reflecting steady wholesale demand. Overall values increased across both major segments, with Cars rising +0.18% and Trucks/SUVs gaining +0.26%, while auction conversion improved to 68%, up two percentage points from the prior week. Trucks and key SUV segments continued to outperform, as buyers remained disciplined and focused on well-conditioned, desirable inventory.

Industry News

- February sales results for the Canadian new car market came in just shy of last year 0.2%, reaching an estimated 122,000 units. With the inclement weather and further uncertainty on trade, the result is more positive than the numbers suggest.

- Results from S&P Global highlight a strong ZEV 4th quarter in 2025. With 12.1% market share, fully electric models led the surge in growth, representing8.0%, while keeping in mind that no federal incentive was scheduled to return to the market. Major ZEV markets ranged from 7.7% in Ontario to 22.5% in B.C.

- Hybrid-electric vehicles represented 17.5% market share in the last quarter of 2025, while they accounted for 17.2% for the full calendar year. This powertrain consists of full and mild hybrids growing from 13.3% just one year before.

- The current conflict in the Middle East is causing gas prices to increase globally. As the United States and Israel attacked Iran over a week ago, it has impacted gas prices sizably, with Canada feeling the effects of almost 20 cents so far. Bringing the national average price from 133.4 to 150 cents in this short time frame.

- Christine Feuell is the latest executive who leaves her stand as Chrysler and Alfa Romeo CEO, departing from Stellantis immediately for personal reasons. Feuell had been with the brand since September 2021 and will be replaced by Matt McAlear who will add these two brands to his current leading position with Dodge.

- After dropping the nameplate once again in 2022, Honda will be bringing the Insight back in the Japanese market as an electric compact crossover, limiting production to 3,000 units.