05.14.2025

Market Insights – 5/13/25

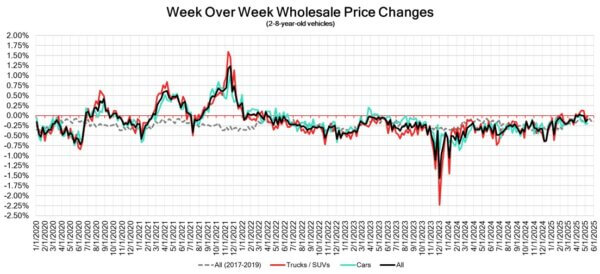

Wholesale Prices, Week Ending May 10th, 2025

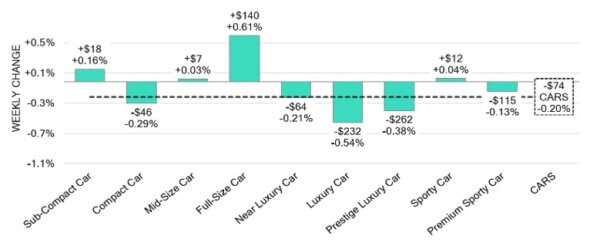

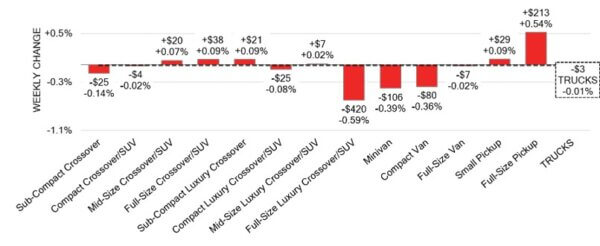

The Canadian used wholesale market saw a decline of -0.10% in pricing for the week. Car segments prices decreased by –0.20% while the Truck/SUV segments decreased by -0.01%. The largest increases were seen in Full Size Car at +0.61% and Full-Size Pickup +0.54%. The largest declines in the Car segments were seen in Luxury Car at -0.54% and Prestige Luxury Car with -0.38%. The largest declines in the Truck/SUV segments were Full Size Luxury Crossover/SUV at -0.59% followed by Minivan with -0.39%.

| This Week | Last Week | 2017-2019 Average (Same Week) | |

| Car segments | -0.20% | -0.21% | -0.10% |

| Truck & SUV segments | -0.01% | -0.09% | -0.09% |

| Market | -0.10% | -0.15% | -0.09% |

Car Segments

- Last week there was an overall downturn of –0.20% seen in car segments. A decline was reflected in five of the nine segments.

- Segments with the largest depreciations were Luxury Car (-0.54%), Prestige Luxury Car (-0.38%) and Compact Car (-0.29%).

- Four segments had an increase in values. Those were Full-Size Car (+0.61%) Sub-Compact Car (+0.16%), Sporty Car (+0.04%) and Mid-Size Car (+0.03%).

Truck / SUV Segments

- There was an overall softening of –0.01%in truck segments last week. This change was reflected in seven of the thirteen segments.

- Segments with the largest depreciations were Full-Size Crossover/SUV (-0.59%), Minivan (-0.39%) and Compact Van (-0.36%).

- Six segments reflected an increase in values. Full-Size Pickup (+0.54%) had the most significant. Full-Size Crossover/SUV, Sub-Compact Luxury Crossover and Small Pickup had the same uptick (+0.09%).

Wholesale

The Canadian market reflected a decrease in pricing, less pronounced than in its prior week. The decline in car segment values decreased by 0.01% down to –0.21%, while truck segments decreased overall by 0.08% bringing its change to -0.01%. Just over 27% of the market segments experienced an average value change of more than ±$100. Monitored auction sale rates ranged from 19.8% to 78.8% averaging at 47.5%. There has been a continuous fluctuation in sale rates across various auction lanes that can be attributed several factors including ongoing political variances and the gradual change in floor prices. Supply has remained high in comparison to prior weeks; however upstream channels continue to gain early access. There continues to be a high demand on both sides of the border for an increase in inventory and vehicles at auctions.

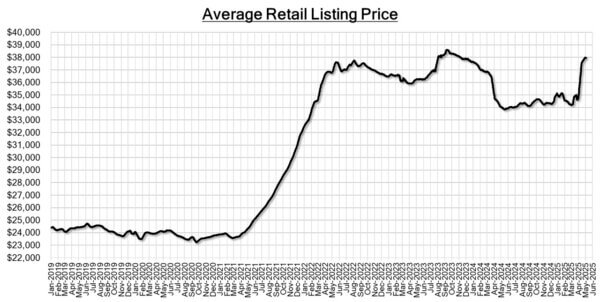

Used Retail Prices & Listing Volume

The average listing price for used vehicles is slightly decreasing, as the 14-day moving average was at $37,950. This analysis is based on approximately 220,000 used vehicles listed for sale on Canadian dealer lots.

Market Insights

Economics & Government

- In April 2025, the S&P Global Canada Services PMI experienced a minor

increase to 41.5, up from 41.2 in the prior month. This marks the fifth consecutive

month of contraction in Canada’s services sector, continuing at a historically rapid

rate. - In March 2025, Canada’s GDP saw a slight increase of 0.1% from the previous

month, as per the preliminary estimates. This growth was driven by

advancements in sectors such as mining, quarrying, oil and gas extraction, retail

trade, and transportation and warehousing. However, this was somewhat offset

by decreases in manufacturing and wholesale trade. - The S&P/TSX Composite Index dropped by approximately 0.4% to below the

24,910 level on Monday, slightly reducing the 1% gain from last week. - The yield on the Canadian 10-year government bond decreased to 3.178%.

- The Canadian dollar is around $0.724 this Monday morning, representing a slight

increase from $0.723 a week prior.

U.S. Market

- The market continues to defy typical seasonal trends, posting a +0.11% increase last week, a notable contrast to the pre-pandemic average for this week, which typically saw a decline of just around -0.20%. Nationwide sales rates remain robust, consistently averaging above 60%, with strong bidder attendance and level of bidding activity.

Industry News

- The United States and United Kingdom have agreed to reduce tariffs on most U.K. vehicle imports with the country now receiving only 10% tariffs on vehicles and an array of parts, initially subject to 25%. Though the improved tariff margin only applies to the first 100,000 units imported into the U.S. (102,000 were imported in all of 2024).

- Scotiabank’s Senior VP, Auto Finance, John Hiscock announced his retirement earlier this year. The 59-year-old industry veteran will be succeeded by John Kontos as of June 2nd. Kontos has been serving as VP, Manufacturer Partnerships and Dealer Programs.

- Toyota may be among one of the largest impacted Auto Manufacturers in the Trump administration’s trade war, with large scale operations within U.S. borders, the brand still requires global parts supply to those facilities causing roughly 1.2 million vehicles to be impacted per year. Toyota has disclosed a nearly $1.2 billion profit drop in only the last 2 months.

- The United States and China have agreed to temporarily lower tariffs. The 145% tariffs on Chinese goods imported to the U.S. will be reduced to 30%, while the 125% on U.S. goods to China will decrease to 10%, all for the next 90-days.

- Nissan Motor Company plans to cut almost 20,000 jobs globally as part of restructuring the business under new CEO, Ivan Espinosa. On top of the already 9,000 planned cuts, this new plan looks add another 10,000 to the total.

- Canadian auto parts manufacturer, Linamar could be one of the only benefactors of the U.S. tariffs, as the company’s parts comply with USMCA rules. Resulting in an acquisition of roughly $200 million in parts contracts in the last quarter.