05.09.2023

Market Insights – 5/9/2023

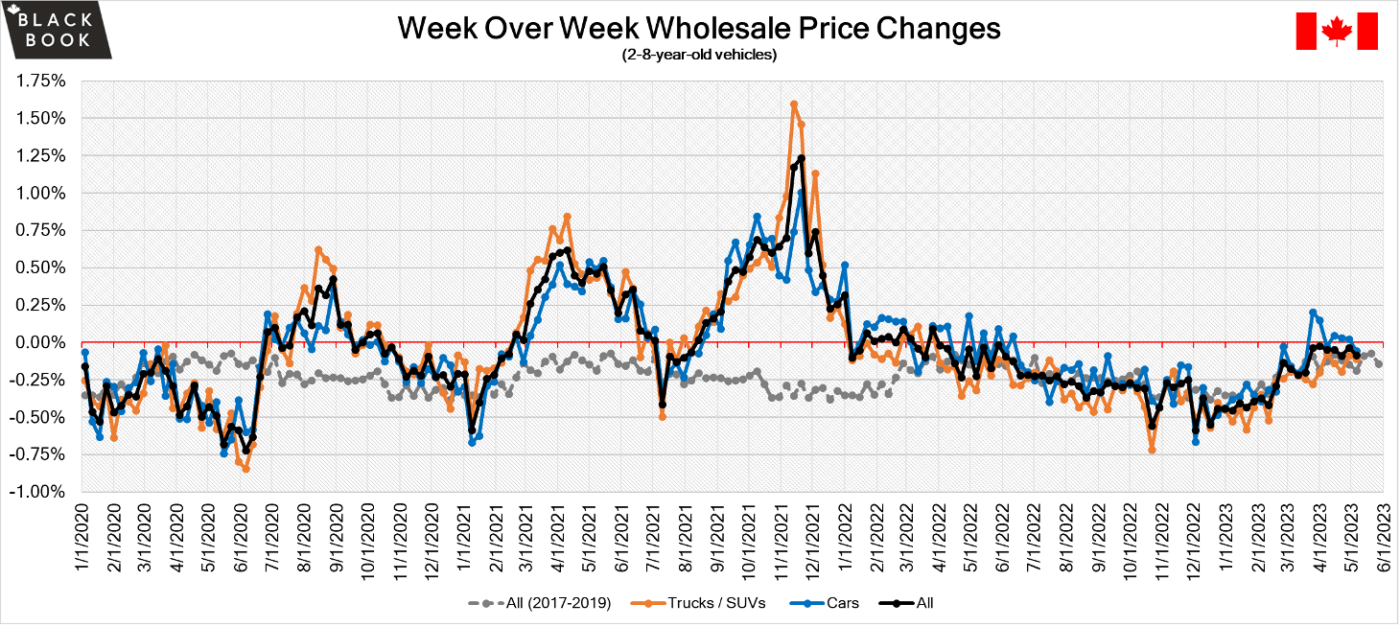

Wholesale Prices, Week Ending May 6th

The Canadian used wholesale market saw a decline in prices for the week at -0.08%. The Car segment fell by 0.06% while Truck/SUVs’ segment prices declined -0.11%. 7 out of 22 segments’ values have increased for the week. Subcompact Cars lead with +0.38 and Compact Cars follow behind at +0.33%. The segments with the largest declines were Prestige Luxury Car (-1.01%) and Compact Van (-0.48%).

| This Week | Last Week | 2017-2019 Average (Same Week) | |

| Car segments | -0.06% | +0.02% | +0.21% |

| Truck & SUV segments | -0.11% | -0.09% | -0.17% |

| Market | -0.08% | -0.04% | -0.19% |

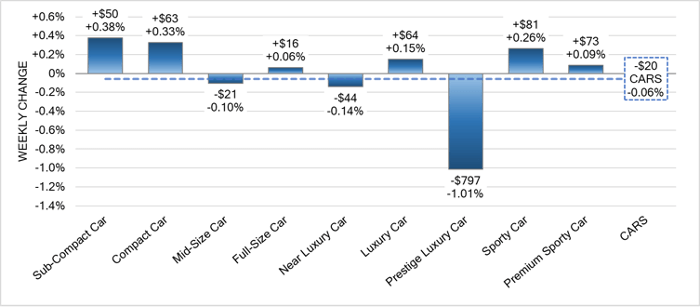

Car Segments

- There was an overall decrease of -0.06% seen in Car segments last week.

- Of the nine, there were six segments with a price increase. Sub-Compact Car had the largest increase at (+0.38%), followed by Compact Car (+0.33%) and Sporty Car (+0.26%).

- The segment with the largest decrease in pricing was Prestige Luxury Cars at (-1.01%).

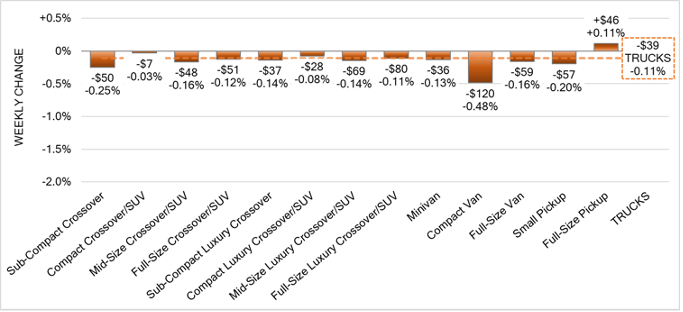

Truck Segments

- Last week overall truck segments decreased on average by -0.11%.

- Segments with the largest declines were Compact Van (-0.48%), Sub-Compact Crossover (-0.25%) and Small Pickup (-0.20%).

- Only one segment experienced an increase. That segment was Full-Size Pickup (+0.11%).

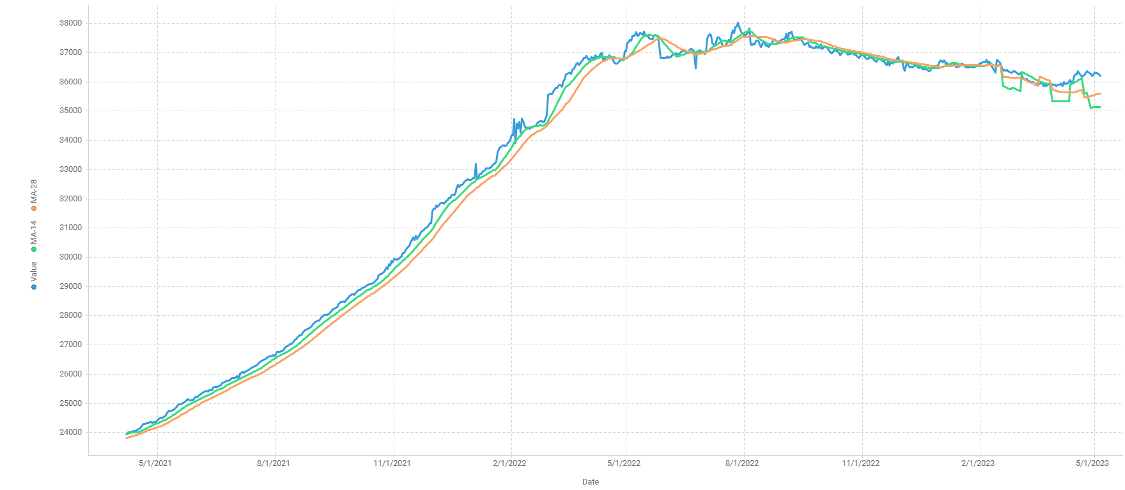

Used Retail Prices & Listing Volumes

The average listing price for used vehicles was consistent week-over-week, as the 14-day moving average was at roughly $35,000. Analysis is based on approximately 175,000 vehicles listed for sale on Canadian dealer lots.

Wholesale

The Canadian market continued to decrease, and the overall decrease was slightly less than the historical average. Supply remains low with high demand for more recent and clean condition vehicles on both sides of the border. Upstream channels continue to tap supply before it can be available to wholesale markets. Many segments saw a change in average value of less than $60 this week as the market continues to stabilize.

Conversion rates were quite varied. Some observed sell rates were as high as 80% but most were in the 40-60% range. Last week we saw more sellers dropping floors, which has been contributing to lanes with higher sell rates.

Canadian Black Book’s Market Insights

Economics & Government

- The unemployment rate in Canada was at 5% for a fifth consecutive month in April of 2023, remaining close to the record-low of 4.9% observed in June and July 2022, and beating market estimates of 5.1%. 41,400 jobs were added in April mor than doubling the market expectations.

- Canada posted a trade surplus of CAD 0.97 billion in March of 2023, above market forecasts of CAD 0.20 billion and swinging from a revised deficit of CAD 0.49 billion in the prior month.

- Exports from Canada fell 0.7% mom to $63.6 billion in March from a downwardly revised $64 billion in the previous period and to the lowest since February 2022, with 8 out of 12 sections in decline.

- The Canadian dollar is around $0.749 this Monday morning showing an increase from $0.738 a week prior.

U.S. Market

In the U.S., overall, Car and Truck segments decreased -0.10% last week; the prior week increased by +0.20%.

Volume-weighted Car segments decreased -0.06%, compared to the prior week’s increase of +0.27%:

- Only three of the nine Car segments increased last week.

- Sporty Car continues to climb, but the rate of increase is slowing with a gain of only +0.39%, compared with the average weekly increase of +0.64% over the past fifteen weeks.

- Prestige Luxury (-0.34%) and Near Luxury (-0.27%) had the largest declines last week, marking the second week in a row of declines for the segments.

Volume-weighted Truck segments decreased by -0.12%; the previous week had an increase of +0.17%:

- Four of the thirteen Truck segments reported increases last week. This was the smallest number of segments reporting an increase since the beginning of February.

- Minivans continue to report positive movements, but the rate of increase is slowing, increasing +0.30% compared with the average weekly gain of +0.74% over the past eleven weeks.

- Pickup trucks, both Small (+0.10%) and Full-Size (+0.09%), continue to increase, but the gains are slowing.

Industry News

- New car sales were only up 2.3% in April compared to year-over-year, as 2023 is quickly becoming a carbon copy of 2022 and 2021, as stated by Desrosiers Automotive Consultants. With April sales lower than the previous month the seasonally adjusted annualized rate (SAAR) now comes in at only 1.48 million units.

- ZEV rebates reached an all-time monthly high in March as deliveries for the month were 9,794, a number larger than January and February combined. With late-breaking price cuts from Tesla and others pushing demand and rebate eligibility up, we’ve seen strong sales for multiple brands selling EV’s.

- Quebec Minister of Environment, Benoit Charette, announced late April that the province is looking to accelerate its yearly ZEV percentage on its road to 100% ZEV mandate by 2035. This increased pace which affects each year prior to 2035, has many industry organizations at odds with the decision while it has started an open and public consultation to the plan over the next 45 days in order for it to pass.

- Stellantis sees Q1 revenue up 14% and cites more normalized inventory levels due to improving semiconductor supply allowing a greater number of sales at higher prices.

- As business operations proceed in a higher interest environment over Q1 2023, AutoCanada revenue was up 15% but profits were down 28% as dealers experience much tighter margins where sales have shifted away from recent record profitability.