06.09.2026

Market Insights – 6/9/26

Wholesale Prices, Week Ending June 6th,2026

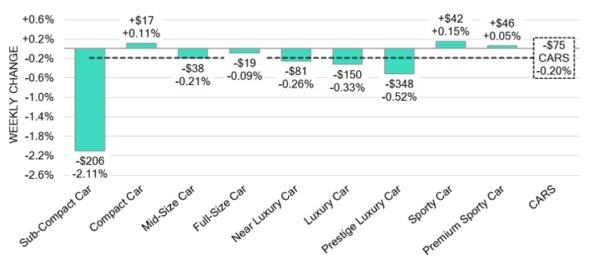

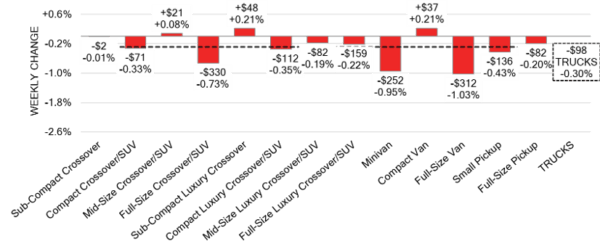

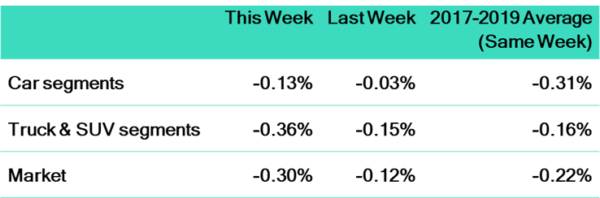

The Canadian used wholesale market saw a decline of -0.25% in pricing for the week. Car segments prices decreased by -0.20% while the Truck/SUV segments decreased by -0.30%. Overall Compact Van segment saw the biggest increase of +0.21%. The largest declines in the Car segments were seen in Sub-Compact Car at -2.11% and Prestige Luxury Car with -0.52%. The largest declines in the Truck/SUV segments were Full-Size Van with -1.03% followed by Minivan at -0.95%.

| This Week | Last Week | 2017-2019 Average (Same Week) | |

| Car segments | -0.20% | -0.37% | -0.14% |

| Truck & SUV segments | -0.30% | -0.58% | -0.17% |

| Market | -0.25% | -0.49% | -0.16% |

Car Segments

- Last week car values softened, with the overall cars market down 0.20%.

- The largest declines came from Sub-Compact Car (-2.11%), Prestige Luxury Car (-0.52%), Luxury Car (-0.33%), and Near Luxury Car (-0.26%).

- The smallest declines were noted in Full-Size Car (-0.09%) and Mid-Size Car (-0.21%).

- Increases were seen in Premium Sporty Car (+0.05%), Compact Car (+0.11%), and Sporty Car (+0.15%).

Truck / SUV Segments

- Last week truck values weakened, with the overall trucks market down 0.30%.

- The largest declines came from Full-Size Van (-1.03%), Minivan (-0.95%), and Full-Size Crossover/SUV (-0.73%).

- The smallest declines were Sub-Compact Crossover (-0.01%), Mid-Size Luxury Crossover/SUV (-0.19%), and Full-Size Pickup (-0.20%).

- Increases were seen in Mid-Size Crossover/SUV (+0.08%), Compact Van (+0.21%), and Sub-Compact Luxury Crossover (+0.21%).

Wholesale

The Canadian market continues its downward trend, with a softer decline compared to last week. Car segment values presented a 0.17% shift, resulting in an overall decline of –0.20%. Truck segment values experienced a 0.28% change, resulting in a cumulative decline of -0.30%. Just under 41% of market segments saw average value movements greater than ±$100.Auction sale rates across watched lanes ranged from 19.2% to 65.7%, resulting in an average of 39.6%. Fluctuations in auction performance continues, driven by seasonal changes, political conditions and sellers standing firm on floor prices. Auction inventory has returned to normal levels; however upstream channels continue to hold priority sale access to inventory. Buyer demand for high-quality vehicles at auctions on both sides of the border persists.

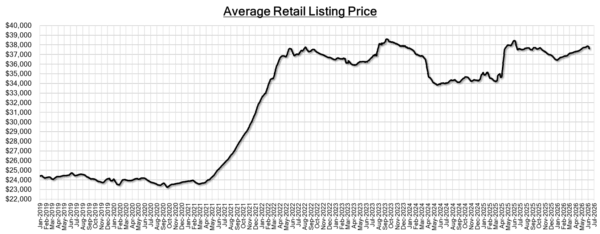

Used Retail Prices & Listing Volume

Market Insights

Economics & Government

- Statistics Canada reported the Unemployment Rate declined to 6.6% in May as

the economy added 87,800 jobs, the largest increase since October 2025. - The Federal Government unveiled its long-awaited AI Strategy, including

measures to provide free training in AI literacy for Canadians and support for

start-up companies in the sector. - The yield on Canadian 10-year government bonds have decreased slightly to

3.31%. - The Canadian dollar is around $0.720 this Monday morning, a slight

decrease from $0.724 a week prior.

U.S. Market

- Wholesale depreciation accelerated modestly last week, driven primarily by weakness across truck and utility segments. On a volume-weighted basis, Car values declined -0.13%, while Trucks/SUVs fell -0.36%, as all thirteen Truck segments posted declines for the first time in twenty-one weeks, ending a prolonged stretch of broad-based strength. Even with values trending lower, auction conversion rates improved to 59%, indicating that vehicles priced in line with market expectations continued to attract solid buyer participation.

Industry News

- May New vehicle sales are down again. With sales at an estimated 184,000 (sourced from Desrosiers Auto Consultants) they remain lower than last year by 1.7% in typically the strongest selling month of the year. Hyundai, Kia, Genesis and Toyota all posted YoY gains, with Hyundai/Genesis setting a company record in May. With those positives, the SAAR came in at only 1.78m.

- The latest tariff developments proposed out of the Trump administration, which could take effect as of July, place a 10-12.5% tariff on countries including Canada, Mexico, Japan, South Korea, China, and the UK/EU that produce auto parts not covered by current tariffs. These would be parts like electronics, interior materials and sub-assemblies, but all under compliance of the CUSMA agreement would be exempt.

- Canadian Dealer Buy-Sells continue with 10 stores changing ownership in May. A common trend only developing further as the general dealer body consolidates and Dealer Groups reconfigure their operations to grow in different market areas.

- Mazda cuts $4,000 off its MSRP to reach under the $50,000 threshold needed for EVAP eligibility on its CX-70/CX-90 plug-in hybrids. Now priced at $48,999 and $49,999 before delivery and fees, respectively.

- The Polestar 2 is returning to Canada, as the Chinese-made EV benefits from the Canada-China tariff deal. It will start delivering 2027MY 2’s in September and account for models in the ‘Year 1’49,000 vehicle quota. Starting price will be $72,700 and achieve the same EPA-range of 447km.

- With a Federal ZEV rebate returned in the form of EVAP, $122m has been claimed in its first 2.5 months, with Toyota claiming 30% of that share. With 7,215 claims it is the number 1 carmaker with GM in 2nd with 3,780.