09.13.2022

Market Insights – 9/13/2022

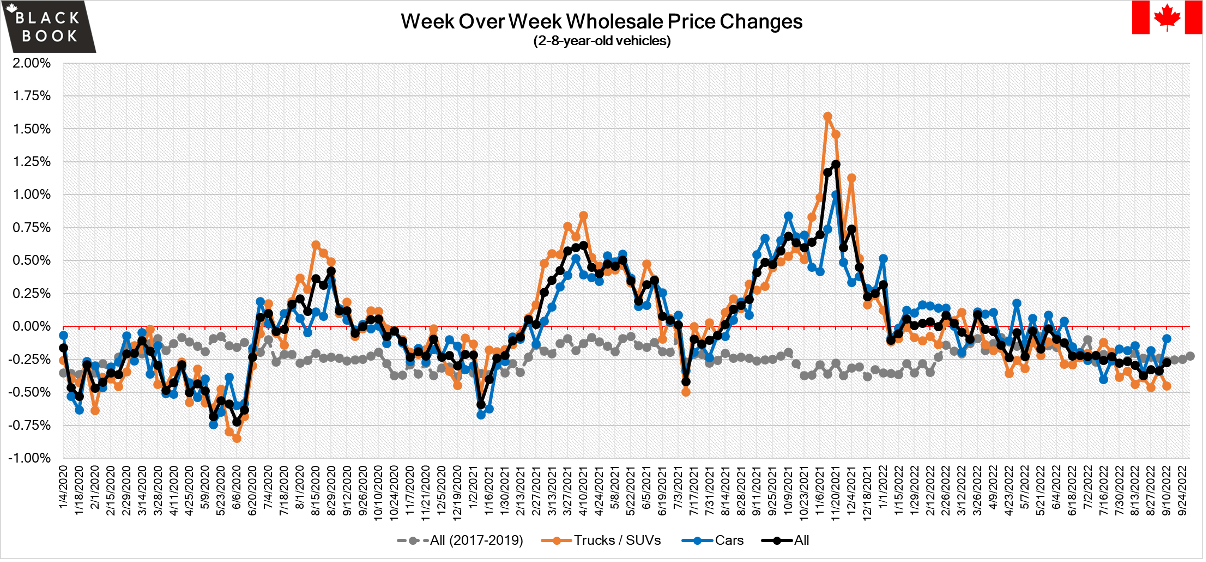

Wholesale Prices, Week Ending September 9th

The Canadian used wholesale market saw prices decline for the week (-0.27%). The Car segment continues to outperform the Truck/SUV segment with a slight decline of –0.09%, while the Truck/SUV segment saw a decline of -0.45%. Of the 22 segments, 8 values have increased for the week. The Full-Size Car segment takes the lead with a +0.91% increase, followed by Minivan at +0.16%. Canada’s wholesale market continues to slow down as markets cool on both sides of the border.

| This Week | Last Week | 2017-2019 Average (Same Week) | |

| Car segments | -0.09% | -0.34% | -0.27% |

| Truck & SUV segments | -0.45% | -0.33% | -0.25% |

| Market | -0.27% | -0.33% | -0.26% |

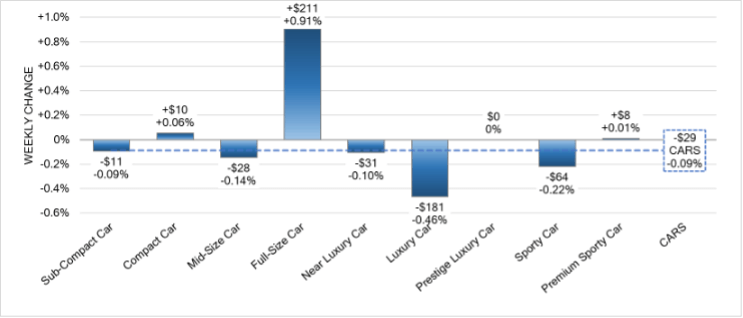

Car Segments

- Car segments decreased on average -0.09% last week.

- Luxury Car segment had the largest drop (-.46%), followed by Sporty Car (-0.22%), Mid-Size Car (-0.14%) and finally Sub-Compact Car (-0.09%).

- Segments with increases were Full-Size Car (+0.91%), next was Compact Car (+0.06%) and lastly, Premium Sporty Car (+0.01%).

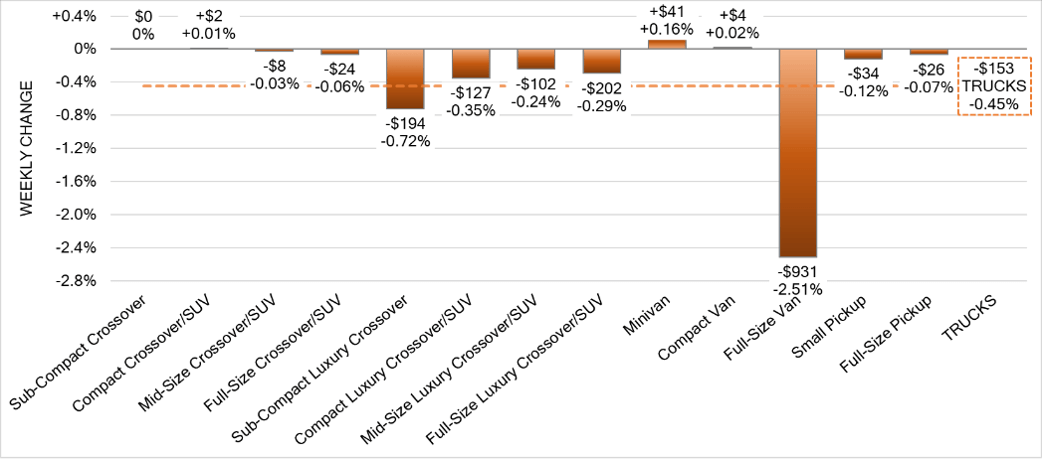

Truck Segments

- Truck segments decreased on average -0.45% last week.

- Full-Size Van had the largest drop (-2.51%), followed by Sub-Compact Luxury Crossover (-0.72%), Compact Luxury Crossover/SUV (-0.35%) and Full-Size Luxury Crossover/SUV (-0.29%).

- Segments with increases were Minivan (+.16%), Compact Van (+0.02%) and Compact Crossover/SUV (0.01%).

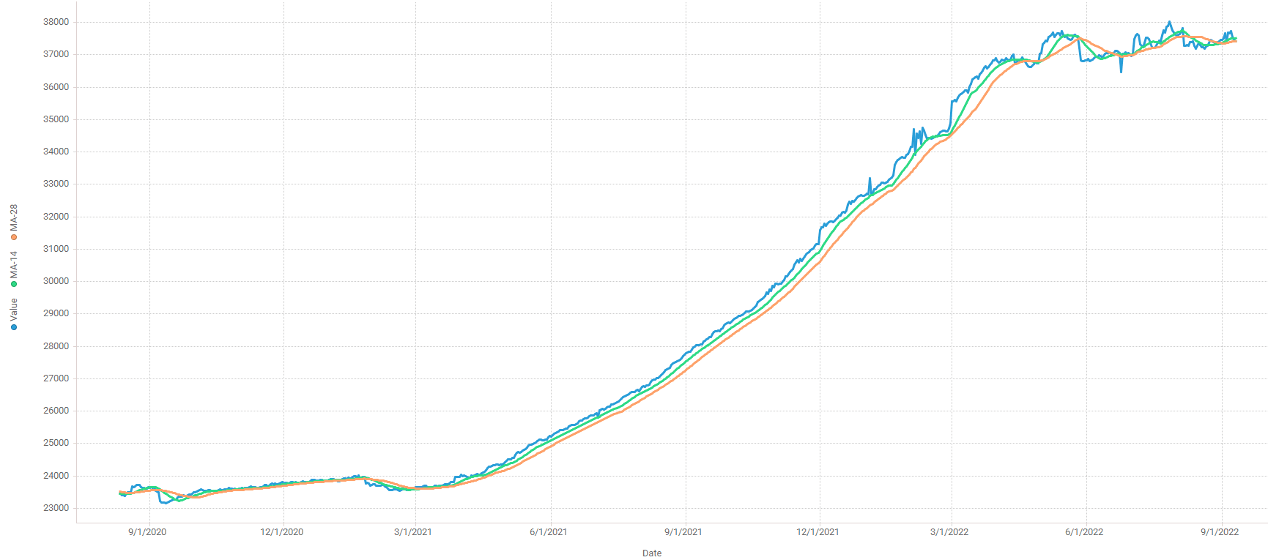

Used Retail Prices & Listing Volumes

The average listing price for used vehicles increased slightly week-over-week, as the 14-day moving average remains stable at roughly $37,500. Analysis is based on approximately 120,000 vehicles listed for sale on Canadian dealer lots.

Wholesale

The Canadian wholesale market decreased further last week. The overall decreases were slightly less than the prior week’s declines. Supply remains low with demand for more recent and clean condition vehicles on both sides of the border. Upstream channels continue to tap supply before it can be available to wholesale markets.

Conversion rates continued to improve last week. Some observed sell rates were as low as 50% but most were in the 60-65% range. This week we are seeing less sellers holding floor prices higher than buyers are willing to go, which has been contributing to lanes with improved sell rates.

The U.S. market exchange rate remains favourable for exportation when price and demand are taken into consideration. Arbitrage opportunities have continued to bring in U.S. buyers, causing a steady flow of vehicles to exit Canada’s wholesale market but slowing as markets cool on both sides of the boarder.

Canadian Black Book’s Market Insights

Economics & Government

- The unemployment rate in Canada rose to 5.4% in August of 2022 from the record-low of 4.9% observed in the previous two months, well above market expectations of 5%. It was the first increase in the jobless rate in seven months, as the number of unemployed individuals rose by 105,900 to 1,113,000 and long-term unemployment rose by 22,000 to make up for the decline in July. On top of that, employment in Canada fell by 39,700 to 19,536,800, marking the third consecutive monthly decline.

- The Bank of Canada raised the target for its overnight rate by 75bps to 3.25% in September 2022, in line with market forecasts. It is the fifth consecutive rate hike, pushing borrowing costs to the highest since 2008. Also, policymakers said interest rates will need to rise further given the outlook for inflation, with surveys suggesting that short-term inflation expectations remain high. The central bank also said it will continue its policy of quantitative tightening.

- The Canadian dollar weakened past the $0.76 mark last week, a level not seen since November 2020, as lingering concerns about slowing economic growth domestically and in the United States, Canada’s primary trade partner, continued to weigh. The market movement came despite another jumbo interest rate hike from the Bank of Canada.

U.S. Market

In the U.S., overall, Car and Truck segments decreased -0.93% last week; the prior week decreased by -0.93%.

Volume-weighted Car segments decreased -0.84%, compared to the prior week’s decrease of -0.95%:

- All nine Car segments decreased last week.

- Full-Size Car had the largest decline last week at-1.21%.

- Luxury Car also had a greater than 1% decline at -1.06%.

- The Sub-Compact Car segment has consistently been the slowest declining segment, but last week the depreciation accelerated, with a single week decline of -0.55%, compared with the prior week’s decline of -0.36%.

Volume-weighted Truck segments decreased by -0.97%; the previous week had a decrease of -0.93%:

- All thirteen truck segments reported decreases.

- Full-Size SUVs (-1.59%) reported the largest truck segment decline last week. The segment has now had nineteen consecutive weeks of declines, with an average weekly change rate of -0.58%.

- Compact and Full-Size Van segments are experiencing softening well below the overall market average, but both segments declined -0.35% last week.

Industry News

- 2024 Chevy Equinox EV will have 400-km range, $35,000 price point while higher-priced trims will offer up to 480 kilometres of range.

- Stellantis extends 2nd shift at Ontario minivan plant until mid-2023; Stellantis said in October 2021 that it would eliminate the second shift in early spring of 2022, but it has since extended the life of the shift three times.

- Lexus RX sales forecasting an increase of 20% as the goal for 2023MY in Canada as it enters its 5th generation, getting a major redesign inside and out.

- Both of Ford Motor Company’s Windsor engine plants have experienced downtime in the past couple of weeks due to various part supply issues unrelated to the ongoing microchip shortage.